Key Takeaways:

Creating an app like BenefitPay requires seamless BENEFIT network integration, strict CBB compliance, and a user-focused design that delivers fast, secure, real-time digital payments for Bahrain.

The cost to develop a digital wallet like BenefitPay ranges from BHD 9,500 to BHD 38,000+ ($25,000 to $100,000+), based on features, security standards, and other factors are the biggest cost drivers.

Major challenges include real-time settlements, strict regulations, and multi-bank integrations, all requiring specialized fintech expertise to build a wallet that performs reliably under national-scale transaction loads.

Bahrain’s booming fintech adoption and strong government support make it the ideal time to launch a BenefitPay-like wallet that captures daily payments, merchant transactions, and long-term user loyalty.

JPLoft stands out by offering end-to-end fintech development with BENEFIT integration, CBB compliance support, bilingual UX, and secure architectures that help you launch a high-performing wallet with confidence.

Want to create a digital wallet like BenefitPay in Bahrain? Digital wallets are transforming payments across the GCC, with Bahrain's fintech market projected to reach USD 1.2 bn.

BenefitPay, Bahrain's leading wallet solution, processes thousands of instant transactions daily through the national BENEFIT network.

Building a similar platform requires three key steps: obtaining a Central Bank of Bahrain (CBB) fintech license, integrating with local payment infrastructure like BENEFIT, and implementing Islamic finance-compliant features for the Bahraini market.

Development typically costs $50,000-$200,000 and takes 6-12 months, depending on features like QR payments, bill splitting, and merchant integrations.

This guide covers regulatory requirements, technical architecture, security standards (PCI-DSS compliance), and market strategies to launch your digital wallet successfully in Bahrain's thriving fintech ecosystem.

Overview of BenefitPay

What makes BenefitPay different from other digital wallets? Launched by Bahrain's national payment gateway operator, Benefit Company, BenefitPay stands as the Kingdom's first homegrown digital wallet with direct integration into the national BENEFIT network.

Unlike generic e-wallet solutions, BenefitPay offers instant bank-to-wallet transfers across all 16 Bahraini banks without intermediary delays.

Key Differentiators:

-

Zero transaction fees for peer-to-peer transfers (unlike PayPal or regional competitors)

-

Instant settlements through direct BENEFIT infrastructure access

-

Government payment integration for utilities, traffic fines, and municipal services

-

Islamic finance compliance is built into the core architecture

When you develop an e-wallet app like BenefitPay, you're essentially creating a nationally integrated payment ecosystem rather than just another wallet.

The platform processes over 2 million transactions monthly, demonstrating how to create an e-wallet app that truly resonates with local market needs through strategic infrastructure partnerships and localized features that global wallets cannot replicate.

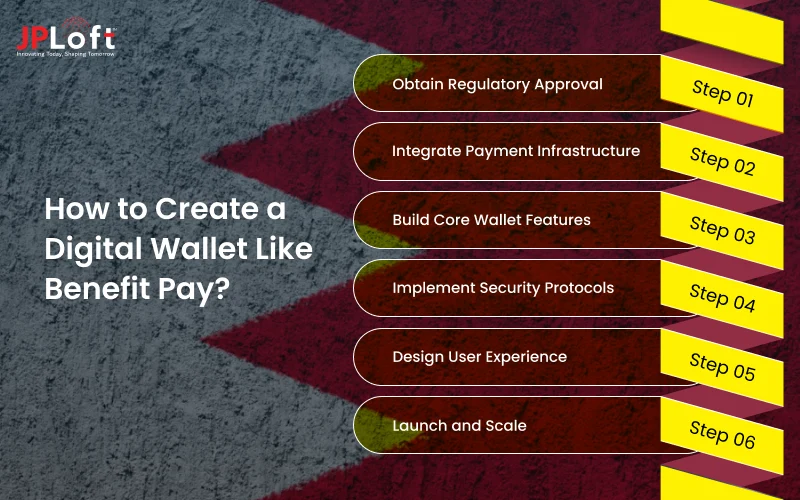

How to Create a Digital Wallet Like Benefit Pay?

Ready to turn your e-wallet app idea into a reality? Well, this is the right time to do so.

To develop a digital wallet like BenefitPay, you need a strategic roadmap that combines regulatory compliance, cutting-edge technology, and a deep understanding of the market.

The process involves navigating Bahrain's fintech-friendly regulations while building a robust infrastructure that can handle millions of transactions securely. BenefitPay's success stems from its seamless integration with national payment systems and user-centric design.

Step 1: Obtain Regulatory Approval

Securing regulatory approval is the cornerstone of your success.

The Central Bank of Bahrain (CBB) offers one of the most advanced fintech frameworks in the Middle East, but strict compliance is essential.

To start, apply for the CBB Regulatory Sandbox Program, which allows you to test your digital wallet, such as when you create an app like BenefitPay, with real users for 6-12 months under supervision.

This sandbox model lets you validate your business while ensuring compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations.

You'll need to provide comprehensive documentation, including your business plan, technical architecture, risk management framework, and financial projections.

Graduating successfully from the sandbox paves the way for obtaining a full Payment Service Provider (PSP) license, empowering you to operate across Bahrain.

Step 2: Integrate Payment Infrastructure

Payment infrastructure integration is what separates regional players from global wallets.

To truly develop a digital wallet like BenefitPay, you must establish direct connectivity with the BENEFIT network, Bahrain's national automated clearing house that processes all interbank transactions.

This integration enables real-time fund transfers across all 16 commercial banks operating in Bahrain, eliminating the 24-48 hour delays typical of international payment processors.

It’s also a foundational requirement for anyone planning to build an ewallet super app that handles high-volume, instant payments reliably.

Partner with BENEFIT Company to access their APIs, which handle instant payments, direct debits, and merchant settlements.

You'll also need to integrate card network APIs from Visa and Mastercard for international transactions, and consider connecting with regional payment gateways like Network International or Checkout.com.

Implementation requires specialized payment gateway developers experienced with ISO 8583 messaging standards and real-time gross settlement systems.

Step 3: Build Core Wallet Features

Your feature set determines market competitiveness.

Start with essential wallet features: secure account creation with digital KYC verification, multi-currency wallet support prioritizing Bahraini Dinar (BHD) alongside major currencies like USD, EUR, and SAR.

Implement a sophisticated QR code payment system that works at merchant point-of-sale terminals and enables contactless transactions.

Develop a comprehensive bill payment gateway connecting to BATELCO (telecom), Electricity and Water Authority (EWA), traffic fine systems, and municipal services. Bahrainis pay an average of 8-12 bills monthly, making this feature critical.

Build peer-to-peer instant transfer capabilities using mobile numbers or email addresses as identifiers, eliminating the need for complex account numbers.

Add transaction categorization, spending analytics, and budget tracking tools that help users manage finances.

When you plan to build a digital wallet like BenefitPay, you should include merchant discovery features showing nearby businesses accepting your wallet.

Plan for future features like split bills, group payments, loyalty rewards integration, and micro-investment options.

Step 4: Implement Security Protocols

Digital wallet security isn't optional; it's existential.

You’re dealing with money, identity, and trust, so every layer of your system must operate beyond banking-grade standards.

If you plan to build a digital wallet like BenefitPay, this level of protection isn’t a bonus. It’s the baseline.

Start by achieving PCI-DSS Level 1 compliance, the highest certification any payment processor can get. It demands annual audits, strict access controls, and continuous monitoring.

Pair that with multi-factor authentication that blends passwords, SMS OTPs, and biometric checks such as fingerprint or Face ID for sensitive actions.

Encrypt everything. Use AES-256 for data at rest and TLS 1.3 for data in transit, making intercepted data useless.

Strengthen this with machine-learning fraud detection that studies spending patterns and flags anything out of character, like odd locations, rapid repeated payments, or sudden spikes in transaction amounts.

Tokenization should replace real card numbers with random tokens, shrinking the blast radius of a breach. Device fingerprinting helps spot unauthorized logins from unfamiliar devices.

Finally, build reliable backup and disaster-recovery systems supported by geographically distributed data centers.

Security isn’t a feature here. It’s the foundation that keeps users safe and your wallet credible.

Step 5: Design User Experience

User experience determines adoption rates. People in Bahrain expect an interface that feels intuitive, fast, and culturally aligned with how they already navigate digital services. This is where strong UI/UX design services make a measurable difference.

Start with a bilingual Arabic-English interface that lets users switch languages instantly. Arabic remains the everyday language for most residents, while English dominates banking and business activity, so both must feel native. Make sure the Arabic side isn’t just mirrored text. True RTL layout support means repositioning icons, navigation, gestures, and spacing so the design feels intentional, not flipped.

Onboarding should take less than three minutes. Keep the flow tight: phone verification, a quick profile, selfie-based identity checks, and bank linking. Before writing a single line of code, map this as an app wireframe so every step feels predictable and frictionless.

Payment flows must be even faster. Bahraini users should be able to scan a QR code and confirm a payment within two taps. Add familiar colors, patterns, and visual cues that connect with local culture while keeping a modern fintech feel. With smartphone usage above 95 percent, your layout must behave perfectly on every screen size.

Once the foundations are clear, translate the wireframes into an app prototype and put it in front of real Bahraini users, young professionals, families, expats, and seniors. Their feedback will expose friction points you won’t spot in a meeting room. The more you test locally, the more naturally your app fits the market.

A wallet that feels “built for Bahrain” doesn’t happen by accident. It comes from thoughtful design choices backed by real user insights.

Step 6: Launch and Scale

Strategic launch determines long-term success.

Begin with a closed beta program inviting 500-1,000 early adopters who provide detailed feedback on functionality, performance, and user experience.

Use this phase to stress-test your infrastructure under real transaction loads and identify bugs before public launch.

Develop a phased rollout strategy: start with core features, then gradually introduce advanced capabilities based on user demand and technical stability.

Build merchant partnerships before public launch; users won't adopt a wallet with nowhere to spend.

Target high-traffic categories: supermarkets, restaurants, petrol stations, and online retailers. Offer merchants competitive transaction fees (1.5-2% vs. 2.5-3% for cards) to incentivize adoption.

Launch aggressive user acquisition campaigns through social media, influencer partnerships, and referral programs offering sign-up bonuses.

Consider a partnership with employers for salary disbursement directly to your wallet, guaranteeing monthly active users.

Monitor key metrics: daily active users (DAU), transaction volume, average transaction value, merchant acceptance, and customer acquisition cost.

Remember: How to develop an app like BenefitPay succeeded through strategic government partnerships and became the default digital payment method for public services.

To keep your app performing at its best, don't overlook the importance of mobile app maintenance services. Regular updates and bug fixes will ensure long-term stability and user satisfaction.

So, this is how to build an app like BenefitPay. With that being said, time to talk about: Features to integrate in an app like BenefitPay.

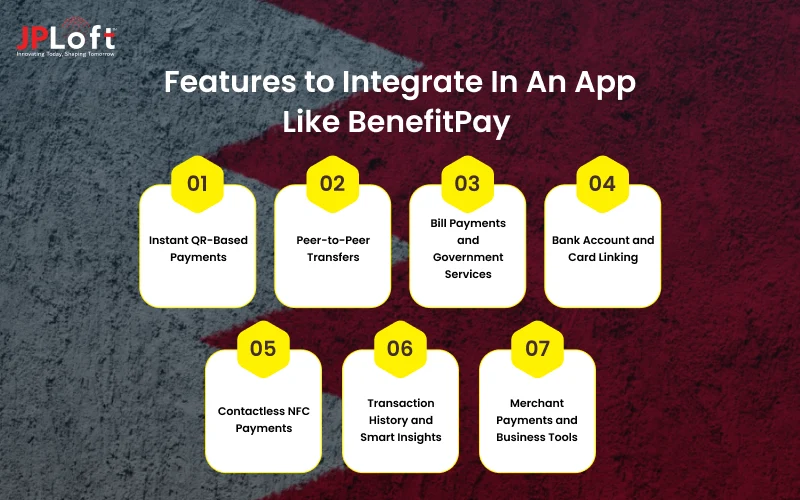

Features to Integrate In An App Like BenefitPay

Building a successful payment app starts with understanding which ewallet app features actually shape daily user behavior.

People want speed, trust, and simplicity, all wrapped in an interface that feels familiar. The stronger and more thoughtful your feature stack is, the faster users adopt and stick with your wallet.

Here are some features that you should explore:

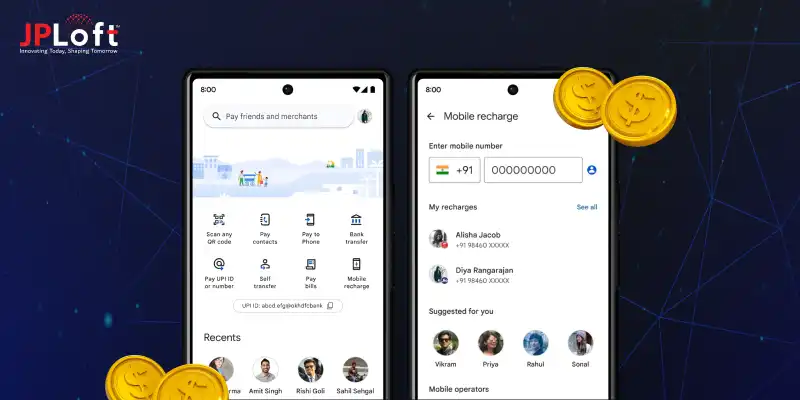

1] Instant QR-Based Payments

QR payments are the heartbeat of BenefitPay. Users scan a code, confirm in seconds, and walk away.

For this to feel effortless, keep the camera activation fast, auto-detect supported codes, and show a crisp confirmation screen.

Add merchant branding, recent payment shortcuts, and low-light scanning support to make it even smoother in real-life situations like cafés, taxis, or retail stores.

2] Peer-to-Peer Transfers

P2P transfers need to feel cleaner than sending a WhatsApp message.

Allow users to search contacts, send money by phone number, and add personal notes. Make recent recipients visible at a glance.

Instant notifications and clear status updates remove anxiety during transfers. A polished experience turns P2P payments into a habit users rely on multiple times a day.

3] Bill Payments and Government Services

This is where a wallet becomes a daily essential.

Let users pay utilities, telecom bills, traffic fines, municipality fees, and school payments from one dashboard.

Add reminders, auto-pay options, and personalized suggestions based on payment history.

When bills feel organized and effortless, users naturally treat your wallet as their default financial touchpoint.

4] Bank Account and Card Linking

Seamless linking builds trust from the very first session.

Support major Bahraini banks, debit cards, credit cards, and prepaid cards.

Keep the UI simple and add real-time validation so users know instantly if a card or account is successfully connected.

The quicker you reduce setup friction, the faster users reach their first transaction.

5] Contactless NFC Payments

NFC adds a premium feel to the payment experience. Let users tap their phone at POS terminals just like a physical card.

The key is speed: the wallet should authenticate instantly with biometrics and complete the transaction without extra screens.

This capability becomes a major advantage when you start an online ewallet business, especially for supermarkets, fuel stations, and other high-footfall locations.

6] Transaction History and Smart Insights

A clean history page builds transparency.

Group transactions by category, merchant, and date. Add filters, search, digital receipts, and small spending insights that help users understand their habits.

When the app feels like a personal finance companion instead of just a payment tool, users open it more often.

7] Merchant Payments and Business Tools

BenefitPay is widely used by local businesses, so give merchants a dedicated section.

Let them generate QR codes, view earnings, process refunds, settle accounts, and track performance.

Adding simple analytics, sales breakdowns, peak hours, or customer trends turns your app into a powerful tool for SMEs and home-based businesses.

So, these are some of the features that you need in your app. With features being aside, knowing the cost is really important.

How Much Does it Cost to Develop an App like BenefitPay in Bahrain?

Let's talk money, because that's probably why you're here, right?

Developing an e-wallet app like BenefitPay isn't cheap, but it's more accessible than you think. The e-wallet app development cost in Bahrain typically ranges from BHD 9,500 to BHD 38,000+ ($25,000 to $100,000+), depending on what you're building.

Think of it like buying a car. You can get a basic model that gets you from A to B, or you can go premium with all the bells and whistles.

The real cost drivers? Features, integrations, and security protocols. A simple peer-to-peer payment app sits at the lower end. But if you want BENEFIT network integration, bill payments, merchant partnerships, QR code systems, and bank-grade security, you're looking at the higher range.

Most Bahraini startups launch with an MVP (Minimum Viable Product) around BHD 10,500-BHD 17,000 ($28,000-$45,000), then scale up based on user feedback.

E-Wallet App Development Cost Breakdown (Bahrain Market)

|

Development Component |

Basic Wallet |

Standard Wallet |

BenefitPay-Level Wallet |

|

Total Cost Range |

BHD 9,500 – BHD 14,000 ($25,000 – $37,000) |

BHD 14,000 – BHD 26,000 ($37,000 – $69,000) |

BHD 26,000 – BHD 38,000+ ($69,000 – $100,000+) |

|

Development Timeline |

3–4 months |

5–7 months |

8–12 months |

|

Core Features |

|

|

|

|

Authentication |

PIN/Password |

2FA + Biometrics |

Multi-factor + Device fingerprinting |

|

Payment Integration |

Third-party gateway |

Card networks + Local banks |

Direct BENEFIT network access |

|

Security Level |

Basic encryption |

PCI-DSS compliance |

Bank-grade + Regulatory sandbox |

|

Backend Infrastructure |

Shared hosting |

Cloud-based (AWS/Azure) |

Enterprise cloud + Redundancy |

|

Design Complexity |

Template-based |

Custom UI/UX |

Bilingual + Cultural customization |

|

2–3 basic APIs |

5–8 payment APIs |

12+ APIs (banks, utilities, govt) |

|

|

Team Size Required |

3–4 developers |

5–7 specialists |

8–12+ full team |

|

Post-Launch Support |

3 months basic |

6 months standard |

12 months+ ongoing |

|

Best For |

Startups testing concept |

Growing fintech companies |

Market leader ambitions |

What Impacts Your E-Wallet App Development Cost?

1. Regulatory eWallet Compliance — BHD 3,800 - BHD 11,400 ($10,000-$30,000)

Getting CBB approval and sandbox participation isn't free. Factor in legal fees and compliance audits.

2. BENEFIT Network Integration — BHD 9,500 - BHD 22,800 ($25,000-$60,000)

This is the game-changer. Direct banking integration costs more but gives you BenefitPay-level performance.

3. Security Infrastructure — BHD 7,600 - BHD 19,000 ($20,000-$50,000)

PCI-DSS certification, encryption, fraud detection—these aren't optional. One breach destroys everything.

4. Design & UX — BHD 5,700 - BHD 13,300 ($15,000-$35,000)

Bahraini users expect bilingual interfaces that feel native. Generic templates won't cut it.

5. Maintenance & Updates — BHD 5,700 - BHD 15,200/year ($15,000-$40,000/year)

Software isn't "build it and forget it." Budget for ongoing improvements, bug fixes, and feature additions.

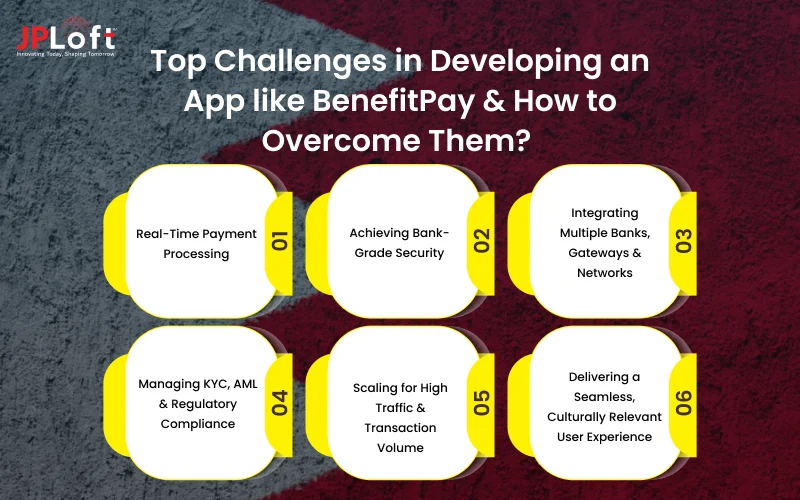

Top Challenges in Developing an App like BenefitPay & How to Overcome Them?

Building a national-level payment platform comes with multiple digital wallet development challenges, from real-time settlements to strict compliance. These challenges shape how you plan, architect, and execute when you decide to create a Digital Wallet, Like BenefitPay.

Here are some challenges & their solutions:

1. Real-Time Payment Processing

Delivering instant payments across all banks is difficult because most conventional payment rails aren’t built for millisecond-level settlement. Coordinating between banks, gateways, and clearing systems becomes even more complex at scale.

If you want to offer instant payments or loyalty rewards, you can integrate an e-wallet in your app to handle secure transactions effortlessly.

Solution: Establish direct connectivity with BENEFIT network APIs and optimize your transaction engine for real-time settlement. This foundation is essential when you aim to develop a digital wallet like BenefitPay that performs reliably under high load.

2. Achieving Bank-Grade Security

Security requirements go far beyond typical apps. Financial platforms must handle sensitive data, prevent fraud, and withstand high-level intrusion risks. Missing any layer of protection can break user trust instantly.

Solution: Implement PCI-DSS standards, tokenization, biometrics, and AI-driven fraud analytics. These layered defenses are mandatory if you plan to make a digital wallet like BenefitPay that users can confidently rely on for daily transactions.

3. Integrating Multiple Banks, Gateways & Networks

Connecting with banks, card networks, and government systems requires handling diverse APIs, inconsistent documentation, and strict uptime expectations. Poor integration causes delays, errors, and user frustration.

Solution: Build a modular integration architecture with sandbox testing and dedicated API specialists. This structure ensures stability during BenefitPay-like app development and minimizes failures across complex financial systems.

4. Managing KYC, AML & Regulatory Compliance

Bahrain mandates strong compliance, including identity verification, AML checks, and secure data flows. Manual processes slow onboarding and create friction for new users.

Solution: Use automated KYC workflows, document scanning, liveness detection, and encrypted data storage. These tools streamline onboarding and keep you compliant as you create a Digital Wallet Like BenefitPay, for a regulated market.

5. Scaling for High Traffic & Transaction Volume

Payment apps face unpredictable traffic spikes, salary days, bill cycles, holiday shopping, or merchant promotions. Slow performance or downtime damages brand credibility instantly.

Solution: Use autoscaling cloud clusters, distributed databases, and multi-zone redundancy. This ensures your platform remains stable and responsive as you grow and develop a digital wallet like BenefitPay for national adoption.

6. Delivering a Seamless, Culturally Relevant User Experience

Bahrain’s audience requires a bilingual interface, real RTL support, and fast payment flows that work for all demographics. Any friction lowers adoption rates.

Solution: Design a user-tested UI with instant QR payments, smooth navigation, and true Arabic-English switching. This approach helps you make a digital wallet like BenefitPay that feels native to local users.

With these challenges in mind, collaborating with a skilled Mobile app development company in US ensures you build the right solution.

Who Can Help You Develop a Secure, Scalable App Like BenefitPay?

Looking for an expert team that actually delivers?

Here's the truth: not every development company can build a BenefitPay-level wallet.

You need a team that understands fintech regulations, banking integrations, and what makes Bahraini users tick.

That's where JPLoft comes in.

We're not just coders throwing together another payment app. We're fintech specialists who've built secure, scalable digital wallets for clients across the Middle East and beyond.

What makes JPLoft different?

We've already solved the hard problems you're about to face.

-

BENEFIT network integration? Done it.

-

CBB regulatory compliance? We know the process inside out.

-

Multi-currency wallets with bank-grade security? That's our specialty.

Our ewallet app development services cover everything from initial concept to post-launch scaling:

-

Regulatory navigation — We handle CBB licensing, sandbox applications, and compliance documentation

-

BENEFIT integration — Direct access to Bahrain's national payment infrastructure

-

Security-first architecture — PCI-DSS compliance, fraud detection, and encryption built in from day one

-

Bilingual UX design — Interfaces that feel native to Bahraini users, not translated templates

-

Scalable cloud infrastructure — Built to handle thousands of transactions from launch day

-

Ongoing support — We don't disappear after deployment.

Here's what you get with JPLoft:

-

15+ years of fintech development experience

-

50+ successful digital wallet and payment app launches

-

24/7 technical support throughout development and beyond

-

Transparent pricing — No hidden fees, no budget surprises

-

Agile development — See progress every two weeks, provide feedback in real-time

We've helped startups go from idea to 100,000+ active users. We've built wallets processing millions in transactions monthly.

Your competition is already building. The question is: will you lead or follow?

Ready to build the next BenefitPay? Let's talk. Get a free consultation and detailed project proposal tailored to your vision.

Conclusion

Building a wallet at the level of BenefitPay isn’t just a development project; it’s a full ecosystem play involving regulations, banking integrations, security layers, and real-time infrastructure.

The cost to develop a digital wallet like BenefitPay depends on how advanced your features are, how deeply you integrate with BENEFIT, and the scale of your user base.

Once the foundations of compliance, architecture, and user experience are in place, your app becomes more than a payment tool; it becomes a financial companion Bahrainis rely on daily.

With the right team, your digital wallet can match and even surpass s, existing players in the market.

FAQs

To develop an app like BenefitPay, you need airtight security, real-time banking integrations, CBB compliance, and a feature-rich user experience that feels built specifically for Bahrain’s payment culture.

Most wallets cost between BHD 9,500 and BHD 38,000+, depending on features, infrastructure, and BENEFIT integration requirements.

Yes, you must apply for the CBB Regulatory Sandbox and later secure a PSP license to operate legally in Bahrain.

Yes, but you must meet technical and security requirements before Benefit grants API access for instant payments and merchant settlements.

A fully integrated wallet typically takes 6–12 months based on complexity, feature set, and regulatory steps.

Savannah is a passionate tech enthusiast with a sharp understanding of client needs across diverse digital domains. With expertise spanning financial platforms, on-demand solutions, and emerging technologies, she brings a unique blend of analytical insight and interpersonal skills, helping businesses decode complexities and make informed decisions in today's rapidly evolving digital world.

Share this blog